Compare Medicare Supplement Plans: G vs F vs N

When people compare Medicare supplement plans 2026 options, the same three letters usually come up first: Plan G, Plan F, and Plan N. They are popular because they can reduce the surprise bills left behind by Original Medicare, but they do not work the same way for every person. The right choice depends on your eligibility, budget, doctor habits, travel plans, and comfort with small out-of-pocket costs.

Confused by your Medicare options? The Big 65 can help you review your Medicare Supplement options at no additional cost to you.

Think of Plan G, Plan F, and Plan N as three versions of the same idea. All three are Medigap policies, which means they work with Original Medicare Parts A and B. They are not Medicare Advantage plans. They do not create a provider network. They are designed to help pay some of the deductibles, coinsurance, and copayments that Original Medicare leaves to you.

That is where many shoppers get stuck. If the benefits are standardized, why are the premiums different? Why can some people buy Plan F while others cannot? And is Plan N really a bargain if it comes with copays and possible excess charges? Let us walk through the differences in plain English.

Quick Answer: Which Medigap Plan Is Usually Best?

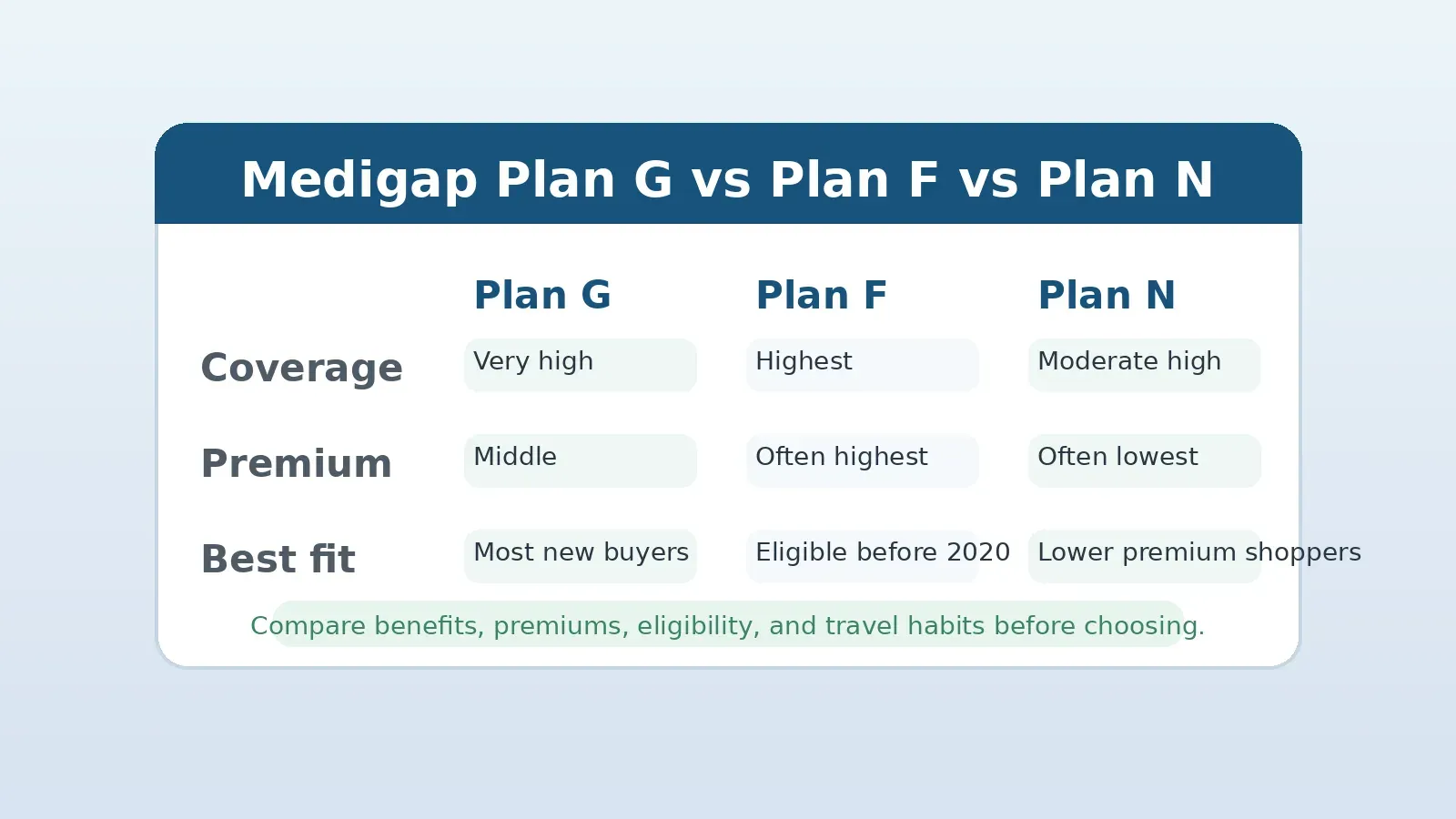

For many people newly eligible for Medicare, Plan G is often the strongest starting point because it offers broad coverage and is available to new Medicare beneficiaries. You pay the Medicare Part B deductible yourself, and after that, Plan G generally covers the remaining Medicare-approved gaps that Plan F would cover.

Plan F can still be excellent for people who were eligible for Medicare before January 1, 2020, because it covers the Part B deductible. However, it is not available to most people who became eligible for Medicare on or after that date. In many markets, Plan F premiums can also be higher, so the extra premium should be compared against the deductible it covers.

Plan N can be a smart fit for someone who wants a lower monthly premium and is comfortable with some cost sharing. With Plan N, you may have office visit copays, emergency room copays if you are not admitted, and you are responsible for Part B excess charges in states where those charges are allowed.

The practical answer is not always “the richest benefits win.” A good decision compares total yearly cost, not just the monthly premium.

Medigap Plan G vs Plan F vs Plan N: Side-by-Side Comparison

| Feature | Plan G | Plan F | Plan N |

|---|---|---|---|

| Available to people newly eligible for Medicare in 2020 or later | Yes | No | Yes |

| Part A hospital deductible | Covered | Covered | Covered |

| Part B deductible | Not covered | Covered if eligible | Not covered |

| Part B coinsurance after deductible | Covered | Covered | Covered, except certain copays |

| Office visit copays | No Plan G copay after Part B deductible | No Plan F copay | Up to $20 for some office visits |

| Emergency room copays | No Plan G copay after Part B deductible | No Plan F copay | Up to $50 if not admitted |

| Part B excess charges | Covered | Covered | Not covered |

| Foreign travel emergency benefit | Included, within plan limits | Included, within plan limits | Included, within plan limits |

| Typical premium level | Middle to high | Often highest | Often lower than G and F |

| Best fit | People who want broad coverage and predictable bills | People eligible before 2020 who want the fullest coverage | People who want lower premiums and can handle some cost sharing |

Medicare Supplement plans are standardized by letter. A Plan G from one carrier has the same basic medical benefits as a Plan G from another carrier in the same state. The premium, rate history, household discounts, underwriting rules, and customer service can still vary by insurance company. That is why comparing only the letter is not enough.

What Plan G Covers and Who It Fits

Plan G is a favorite among people who want strong Medigap coverage without needing to qualify for Plan F. It covers many of the major gaps left by Original Medicare, including the Part A hospital deductible, Part A coinsurance, skilled nursing facility coinsurance, Part B coinsurance, Part B excess charges, and foreign travel emergency benefits within plan limits.

The key item Plan G does not cover is the Medicare Part B deductible. Once you have paid that deductible for the year, Plan G is designed to pick up the Medicare-approved gaps it covers. For someone who wants predictable costs and broad freedom to see doctors who accept Medicare, that can be a very comfortable structure.

Plan G may fit you if:

- You are turning 65 or newly leaving employer coverage.

- You want to keep Original Medicare rather than enroll in a Medicare Advantage plan.

- You travel or spend time in more than one state.

- You want protection from Part B excess charges.

- You prefer fewer copay decisions when you see the doctor.

If you are still comparing the bigger decision of Original Medicare plus a Supplement versus Medicare Advantage, start with this guide to Medicare Advantage vs Medicare Supplement plans. That choice comes before choosing a Medigap letter.

What Plan F Covers and Why Eligibility Matters

Plan F has historically been known as the most comprehensive standardized Medigap plan because it covers the Part B deductible in addition to the other major Original Medicare gaps. For people who like the idea of very limited out-of-pocket bills for Medicare-approved services, Plan F can be appealing.

But there is a major eligibility rule. If you became eligible for Medicare on or after January 1, 2020, you generally cannot buy a new Plan F. If you were eligible for Medicare before that date, you may still be able to apply for Plan F, depending on state rules, underwriting, and carrier availability.

The important question is whether Plan F is worth the premium difference. If Plan F costs much more per year than Plan G, and the main added benefit is payment of the Part B deductible, Plan G may be the better value. In other situations, an existing Plan F policyholder may prefer to stay put because switching could require medical underwriting.

Plan F may fit you if:

- You were eligible for Medicare before January 1, 2020.

- You already have Plan F and your premium remains competitive.

- You value the highest level of standardized Medigap coverage.

- You do not want to handle the Part B deductible separately.

Before changing a Plan F policy, talk through the tradeoffs. A lower premium can look attractive, but underwriting rules can make it hard to move back later.

What Plan N Covers and Where the Savings Come From

Plan N is often attractive because the monthly premium may be lower than Plan G or Plan F. That lower premium comes with a few tradeoffs. You still get strong Medigap coverage, including the Part A hospital deductible and Part B coinsurance, but you agree to some cost sharing.

With Plan N, you may pay up to $20 for some office visits and up to $50 for an emergency room visit if you are not admitted as an inpatient. Plan N also does not cover Part B excess charges. An excess charge can happen when a provider who accepts Medicare but does not accept Medicare assignment charges more than the Medicare-approved amount, within allowed limits.

Some states limit or prohibit excess charges, and many doctors accept Medicare assignment. Still, this detail matters if you see specialists, travel often, or live in an area where excess charges are more common.

If you would like a second set of eyes on Plan G, Plan F, and Plan N rates in your state, call The Big 65 at 877-850-0211 or email Gray@TheBig65.com.

Plan N may fit you if:

- You want a lower monthly premium.

- You do not visit doctors frequently.

- Your doctors accept Medicare assignment.

- You are comfortable paying small copays when they apply.

- You understand the excess charge rule in your state.

Plan N is not automatically better because it is cheaper. It is better only if the premium savings outweigh the copays and possible excess charge exposure for your real life.

How to Compare the True Cost of Plan G, Plan F, and Plan N

A common mistake is choosing the plan with the lowest premium without estimating total yearly cost. The better method is to compare three numbers:

- Annual premium: Multiply the monthly premium by 12.

- Expected out-of-pocket costs: Include the Part B deductible, likely copays, and any exposure to excess charges.

- Risk comfort: Decide how much uncertainty you are willing to accept for a lower premium.

Here is a simple example. If Plan G costs $25 more per month than Plan N, that is $300 more per year. If Plan N saves $300 in premium but you expect several specialist visits, possible copays, and worry about excess charges, the savings may not feel worth it. If you rarely see doctors and your providers accept Medicare assignment, Plan N could still make sense.

For Plan F, compare the annual premium difference against the Part B deductible. If Plan F costs several hundred dollars more than Plan G, you may be paying more in premium than the deductible benefit is worth. The math changes by state, age, household discount, tobacco status, and carrier.

This is also why state-specific pricing matters. The best Medigap choice in Iowa may not be the same as the best Medigap choice in Florida, Alabama, Kentucky, or Colorado. The benefits are standardized, but the premiums are local.

Doctor Access, Travel, and Lifestyle Questions

Medigap plans are popular with people who want the flexibility of Original Medicare. In general, you can see any provider in the United States who accepts Medicare and is accepting new patients. That can be especially useful if you split time between states, travel often, or want access to specialists without a plan network.

Ask yourself these questions before choosing:

- Do I want the freedom to see Medicare providers in multiple states?

- Do I see specialists often?

- Do my doctors accept Medicare assignment?

- Would small copays bother me, or would I rather pay a lower premium?

- Am I eligible for Plan F, or should I focus on Plan G and Plan N?

- How much would a premium increase affect my budget in future years?

If you are changing from Medicare Advantage to Medigap, the timing and health questions can be especially important. Read more about whether you can switch to Medigap without underwriting before assuming the move will be automatic.

When Plan G Is the Better Choice

Plan G is often the better choice when you want broad coverage, eligibility is straightforward, and the premium is reasonable compared with Plan N. It is also a strong choice if you want coverage for Part B excess charges or you prefer not to think about office visit copays.

Someone who sees multiple specialists, travels frequently, or values predictability may find Plan G easier to live with. The premium may be higher than Plan N, but the plan design is simpler. You pay the Part B deductible, then the covered gaps are generally handled by the policy.

Plan G can also be a practical alternative for someone who likes Plan F but is not eligible to buy it. For most new Medicare beneficiaries, the real comparison is Plan G versus Plan N.

When Plan F Is the Better Choice

Plan F can be the better choice for a person who is eligible, wants the most comprehensive standardized Medigap benefits, and finds a premium that still makes sense. It can also be worth keeping if you already have it and switching would create underwriting concerns.

However, do not assume Plan F is always the best value just because it covers more. A plan can have richer benefits and still be overpriced for your situation. Compare the annual premium difference, your health, your state rules, and whether you could qualify for another plan if you applied.

When Plan N Is the Better Choice

Plan N can be the better choice when the premium savings are meaningful and the tradeoffs are manageable. It can work well for someone who wants the flexibility of Original Medicare but does not want to pay for the richest Medigap option.

The best Plan N shoppers usually understand two things. First, lower premium does not mean no out-of-pocket costs. Second, provider assignment and excess charges should be checked before enrolling. If those details look good, Plan N can be a balanced option.

For a broader view of Medicare plan timing, this 2026 Medicare enrollment guide explains when plan changes may be available and why deadlines matter.

Do You Also Need a Part D Drug Plan?

Yes, if you choose Original Medicare with a Medigap plan, you usually need a separate Medicare Part D prescription drug plan. Medigap Plan G, Plan F, and Plan N do not include outpatient prescription drug coverage. That is different from many Medicare Advantage plans, which often bundle medical and drug coverage together.

This is one of the biggest practical differences between Original Medicare with Medigap and Medicare Advantage. With Medigap, you often choose three pieces: Original Medicare, a Supplement plan, and a Part D drug plan. With Medicare Advantage, you may choose one plan that combines several parts, but you also need to pay close attention to networks and plan rules.

If prescription costs are a major concern, include Part D in your total cost comparison. A lower Medigap premium does not help much if the drug plan is wrong for your medications.

A Simple Decision Framework

Use this framework if you are stuck between Plan G, Plan F, and Plan N:

- Confirm eligibility. If you were not eligible for Medicare before January 1, 2020, remove Plan F from your new-policy choices.

- Price the plans in your state. Compare at least several carriers, not just one familiar name.

- Estimate annual cost. Include premiums, deductible responsibility, copays, and likely medical usage.

- Review provider habits. Frequent specialists may make Plan G more attractive than Plan N.

- Check travel needs. Original Medicare with Medigap can be useful for people who want national provider flexibility.

- Think long term. Rate increases, underwriting, and future health changes can matter as much as this year’s premium.

For people turning 65, the first enrollment window can be especially valuable because Medigap underwriting is usually more favorable during the Medigap Open Enrollment Period. If you are approaching Medicare, review this resource for people turning 65 and choosing a Medicare plan.

Bottom Line: Compare Benefits and Premiums Together

Plan G, Plan F, and Plan N are all strong Medicare Supplement options, but they serve different priorities. Plan G is often a balanced choice for broad coverage. Plan F can be excellent for people who are eligible and comfortable with the premium. Plan N can be attractive for people who want lower monthly costs and accept some cost sharing.

The best plan is the one that fits your doctors, budget, state, travel habits, and tolerance for surprise bills. Do not choose based on a letter alone. Compare the total cost, understand the tradeoffs, and make sure the plan supports how you actually use healthcare.

Need help comparing Plan G, Plan F, and Plan N? The Big 65 helps people compare Medicare Supplement plans, Medicare Advantage options, and Part D drug plans. There is no additional charge for the service, and you can call 877-850-0211 to start the conversation.

The Big 65 is an independent Medicare insurance brokerage with more than 20 years of experience helping people make sense of Medicare. The company represents multiple insurance organizations and provides ongoing support, including annual plan reviews, so you are not left to figure out Medicare alone.

Not Sure Which Medicare Plan Is Right for You?

Medicare is complicated, but you do not have to figure it out alone. With over 20 years of experience, Karl Bruns-Kyler can help you compare plans, avoid costly mistakes, and find the coverage that fits your needs and budget.

Call (877) 850-0211

Or schedule a free consultation at a time that works for you.

There is never a charge for my services. Your premium is the same whether you work with me or go direct.

Disclaimer: We do not offer every plan available in your area. Currently, we represent 10 organizations that offer 50 products in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.