Understanding Medicare Supplement (Medigap) Plans in 2026

If you’re turning 65 or already on Original Medicare, you’ve probably noticed that Medicare doesn’t cover everything. The 20% coinsurance on Part B services, the $1,736 Part A hospital deductible, and skilled nursing costs can add up quickly.

That’s where Medicare Supplement Insurance, commonly called Medigap, comes in. These standardized plans sold by private insurance companies help cover the gaps in Original Medicare, giving you more predictable healthcare costs and greater peace of mind.

👉 Need help choosing a Medicare Supplement plan? Talk to an expert at The Big 65 today.

This guide breaks down every Medigap plan available in 2026, compares the most popular options head-to-head, and provides a framework to help you decide which plan may work best for your situation.

Expert Insight: “After helping Medicare beneficiaries across 33 states for over 20 years, the most common mistake I see is people choosing a plan based solely on premium cost without considering their total potential out-of-pocket exposure,” says Karl Bruns-Kyler, founder of The Big 65 Medicare Insurance Services.

All 10 Standardized Medigap Plans: What Each One Covers

The federal government standardizes Medigap plans so that each plan letter (A through N) offers the same benefits regardless of which insurance company sells it. The only difference between carriers is the price you pay. Here is a complete overview of what each plan covers in 2026:

Medigap Benefits Comparison Chart (2026)

| Benefit | A | B | C* | D | F* | G | K | L | M | N |

|---|---|---|---|---|---|---|---|---|---|---|

| Part A coinsurance & hospital costs (up to 365 extra days) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Part B coinsurance or copayment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓** |

| Blood (first 3 pints) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Part A hospice care coinsurance | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Skilled nursing facility coinsurance | ✗ | ✗ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Part A deductible ($1,736 in 2026) | ✗ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | 50% | ✓ |

| Part B deductible ($283 in 2026) | ✗ | ✗ | ✓ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ |

| Part B excess charges | ✗ | ✗ | ✗ | ✗ | ✓ | ✓ | ✗ | ✗ | ✗ | ✗ |

| Foreign travel emergency (80%) | ✗ | ✗ | ✓ | ✓ | ✓ | ✓ | ✗ | ✗ | ✓ | ✓ |

| Out-of-pocket limit | N/A | N/A | N/A | N/A | N/A | N/A | $8,000 | $4,000 | N/A | N/A |

*Plans C and F are not available to people who became newly eligible for Medicare on or after January 1, 2020. If you had Medicare before that date, you may still be able to enroll in these plans.

**Plan N pays 100% of Part B coinsurance except for a copayment of up to $20 for some office visits and up to $50 for emergency room visits that don’t result in an inpatient admission.

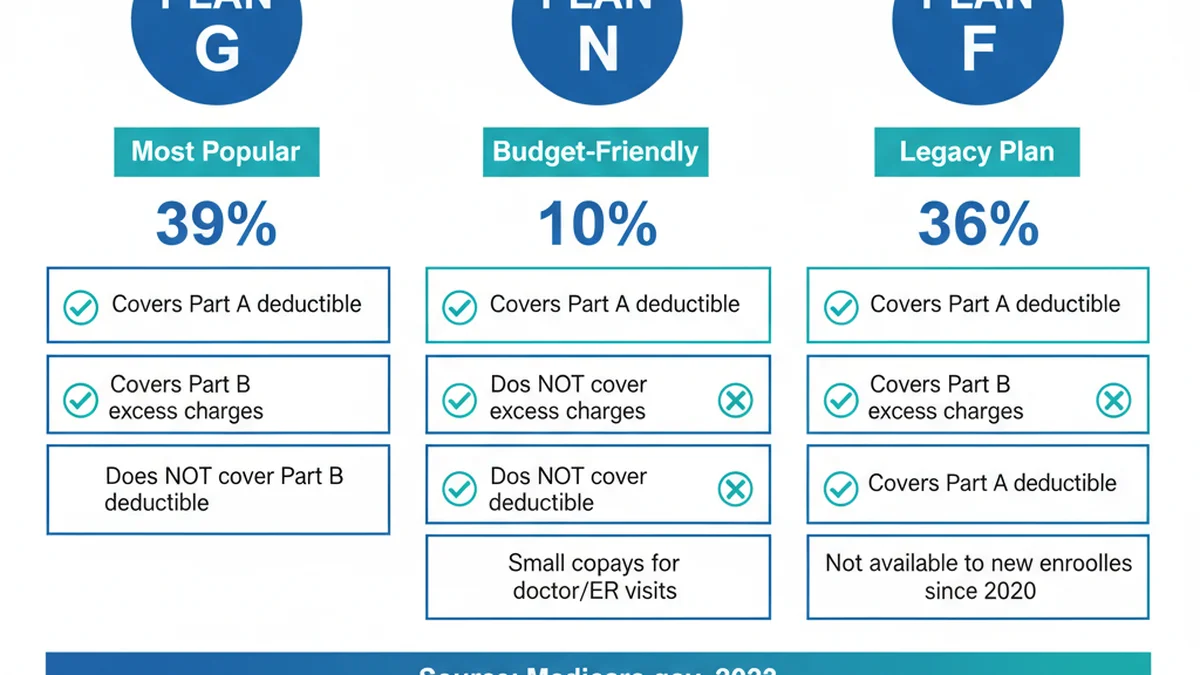

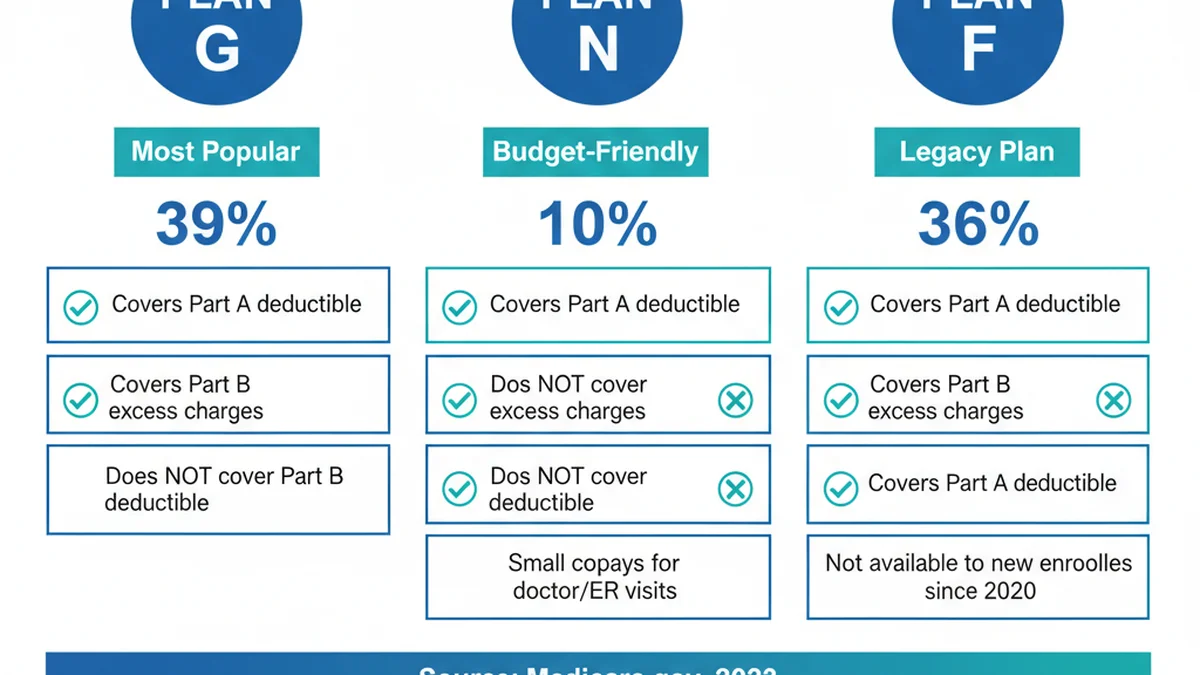

The 3 Most Popular Medigap Plans: Plan G vs. Plan N vs. Plan F

While 10 plans exist, three dominate the market. According to recent enrollment data, Plan G (39%), Plan F (36%), and Plan N (10%) together account for approximately 85% of all Medigap enrollees. Here’s how they compare head-to-head:

Plan G: The Most Popular Choice for New Enrollees

Plan G has become the go-to Medigap plan for people new to Medicare. It covers nearly everything Original Medicare doesn’t, with one exception: the annual Part B deductible ($283 in 2026).

What Plan G covers:

- Part A hospital coinsurance and costs for an additional 365 days after Medicare benefits run out

- Part B coinsurance or copayment (100%)

- First 3 pints of blood

- Part A hospice care coinsurance

- Skilled nursing facility coinsurance

- Part A deductible ($1,736 in 2026)

- Part B excess charges

- Foreign travel emergency coverage (80%)

Why it’s popular: Plan G offers the most comprehensive coverage available to new Medicare enrollees (post-2020). Your maximum out-of-pocket exposure beyond premiums is just $283 per year, making healthcare costs extremely predictable.

Learn more about Medicare Supplement Plan G costs →

Plan N: The Budget-Friendly Alternative

Plan N offers strong coverage at a lower monthly premium than Plan G. The trade-off is small copayments for certain services and responsibility for Part B excess charges (increasingly rare as fewer doctors opt out of Medicare assignment).

Key differences from Plan G:

- Does not cover Part B excess charges

- Requires a copayment of up to $20 for some office visits

- Requires a copayment of up to $50 for ER visits that don’t result in hospital admission

- Does not cover the Part B deductible ($283 in 2026)

Why it appeals to some beneficiaries: The lower premium can save $30-$60 per month versus Plan G. If your providers accept Medicare assignment, Plan N may offer good value.

Plan F: The Legacy Plan (Pre-2020 Enrollees Only)

Plan F is the only Medigap plan that covers all nine standardized benefits, including the Part B deductible. However, Plan F is closed to anyone newly eligible for Medicare on or after January 1, 2020.

If you already have Plan F, you can keep it. But as the Plan F enrollment pool ages and shrinks, premiums may increase more rapidly over time compared to Plan G.

Plan F vs. Plan G: The only coverage difference is the $283 annual Part B deductible. Plan G premiums are often significantly lower, meaning premium savings may more than offset the deductible.

See our detailed Plan G vs. Plan N comparison →

Head-to-Head Comparison: Plan G vs. Plan N vs. Plan F

| Feature | Plan G | Plan N | Plan F* |

|---|---|---|---|

| Part B deductible covered | ✗ | ✗ | ✓ |

| Part B excess charges covered | ✓ | ✗ | ✓ |

| Office visit copays | None | Up to $20 | None |

| ER copay (no admission) | None | Up to $50 | None |

| Foreign travel emergency | 80% | 80% | 80% |

| Available to new enrollees (post-2020) | ✓ | ✓ | ✗ |

| Typical monthly premium range* | $120–$250 | $80–$200 | $150–$300+ |

| Annual out-of-pocket beyond premiums | $283 max | $283 + copays | $0 |

| Enrollment share | 39% | 10% | 36% |

*Premium ranges are approximate national averages and vary significantly by age, location, gender, tobacco use, and insurance carrier. Actual rates in your area may be higher or lower.

Which Medigap Plan May Be Right for You?

There is no single “best” Medigap plan for everyone. The right choice depends on your individual circumstances. Here’s a framework to help guide your decision:

You may prefer Plan G if:

- You want the most comprehensive coverage available to new enrollees

- You value predictable costs and minimal out-of-pocket surprises

- You’re willing to pay a slightly higher premium for peace of mind

- You travel internationally and want emergency coverage abroad

- You became eligible for Medicare on or after January 1, 2020

You may prefer Plan N if:

- You want strong coverage at a lower monthly premium

- You don’t mind paying small copays for office and ER visits

- Your doctors accept Medicare assignment (minimizing excess charge risk)

- You’re generally healthy and don’t visit the doctor frequently

- Monthly premium savings matter to your budget

You may prefer Plan F if:

- You were eligible for Medicare before January 1, 2020, and want zero out-of-pocket costs

- You prefer the simplicity of having every single gap covered

- You’re willing to pay a higher premium for the convenience of $0 cost-sharing

You may prefer Plans K or L if:

- You want the lowest possible monthly premium

- You’re comfortable with cost-sharing up to a defined annual limit ($8,000 for Plan K or $4,000 for Plan L in 2026)

- You want catastrophic protection with a built-in out-of-pocket cap

2026 Medigap Premium Costs: What to Expect

Medigap premiums vary based on several factors, and understanding how insurers price their plans can help you find the best value:

Factors That Affect Your Premium

- Your age: Premiums generally increase as you get older

- Where you live: Rates vary significantly by state and even by county

- Gender: Women often pay lower premiums than men

- Tobacco use: Smokers typically pay higher premiums

- The insurance company: Same benefits, different prices. Always compare carriers.

Three Pricing Methods Insurers Use

- Community-rated: Everyone pays the same premium regardless of age. Premium won’t increase due to aging.

- Issue-age-rated: Premium is based on your age when you buy the policy. Won’t increase due to aging, but may rise for inflation.

- Attained-age-rated: Premium starts lower but increases as you age. Most common method; can lead to significantly higher costs over time.

2026 Average Monthly Premium Estimates by Plan

| Plan | Estimated Monthly Premium Range (Age 65) | Coverage Level |

|---|---|---|

| Plan A | $75–$200 | Basic |

| Plan B | $100–$225 | Basic + Part A deductible |

| Plan C* | $150–$300 | Comprehensive (legacy only) |

| Plan D | $100–$225 | Moderate |

| Plan F* | $150–$300+ | Most comprehensive (legacy only) |

| Plan G | $120–$250 | Most comprehensive (new enrollees) |

| Plan K | $40–$100 | Cost-sharing with $8,000 OOP cap |

| Plan L | $60–$140 | Cost-sharing with $4,000 OOP cap |

| Plan M | $100–$200 | Moderate |

| Plan N | $80–$200 | Strong with small copays |

Premium ranges are national estimates for a 65-year-old non-smoker. Your actual premium depends on your location, gender, health status, and carrier. Compare Medicare Supplement costs in your area for personalized quotes.

Top Medicare Supplement Insurance Carriers in 2026

Since Medigap benefits are standardized, choosing a reputable insurance carrier with competitive pricing and strong customer service matters. Here are some of the most widely recognized carriers offering Medigap plans nationwide:

Major carriers include Mutual of Omaha (one of the largest Medigap providers with competitive Plan G and Plan N rates), Aetna (a national insurer with broad state availability), Cigna (competitive pricing in select states), Blue Cross Blue Shield (affiliates in every state with strong brand recognition), and United American Insurance Company (competitive rates especially in southern and midwestern states).

Important: Every carrier offers the same standardized benefits for a given plan letter, so the right carrier often comes down to the best rate in your zip code and age bracket.

Read our guide to the best Medigap insurance companies →

State Availability and Exceptions

While Medigap plans are standardized at the federal level, there are state-specific considerations to keep in mind:

- Massachusetts, Minnesota, and Wisconsin have their own Medigap standardization systems with different plan names and benefit structures.

- Not all plans are available in every state. Plans A and B must be offered by any Medigap seller, but others (like M or D) may not be available in your area.

- State regulations affect pricing. Some states require community-rated pricing; others allow attained-age rating, which significantly affects long-term costs.

- Guaranteed issue rights vary by state. Some states offer protections beyond the federal minimum.

The Big 65 is licensed to provide Medicare guidance in 33 states, helping beneficiaries navigate the specific plans and carriers available where they live.

The Medigap Open Enrollment Period: Why Timing Matters

Your Medigap Open Enrollment Period (OEP) is the single most important window for purchasing a Medigap plan. It begins the first day of the month you turn 65 and are enrolled in Medicare Part B, and lasts for 6 months.

Why the OEP is critical:

- Guaranteed issue: During your OEP, insurance companies cannot deny you coverage or charge you more because of pre-existing health conditions.

- Best rates: You’ll qualify for the lowest available premiums during this window.

- No medical underwriting: You don’t need to pass a health screening to get coverage.

What happens if you miss the OEP?

After your OEP closes, insurance companies in most states can deny your application, charge higher premiums, or impose waiting periods for pre-existing conditions.

Bottom line: If you’re approaching 65, don’t delay your Medigap research. The decisions you make during your OEP can affect your coverage options and costs for years to come.

Read our complete Medicare Supplement guide for more details →

How to Choose the Right Medigap Plan: A Step-by-Step Framework

- Evaluate your healthcare needs. How often do you visit the doctor? Do you have chronic conditions or anticipate hospitalizations?

- Assess your budget. Higher premium for lower out-of-pocket costs, or lower premiums with some cost-sharing?

- Understand the coverage differences. Use the comparison chart above to see exactly what each plan covers.

- Compare carriers in your area. Benefits are standardized, so focus on price, financial stability, and service ratings.

- Consider the pricing method. Attained-age may be cheaper today but cost more in 10 years. Community-rated offers predictable long-term costs.

- Don’t forget Part D. Medigap plans do not cover prescription drugs. You’ll need a separate Medicare Part D plan for drug coverage.

- Enroll during your OEP. Maximize your guaranteed issue rights and get the best available rates.

- Work with an independent advisor. An independent Medicare advisor (not tied to a single carrier) can compare plans and rates across multiple companies on your behalf.

Medicare Supplement vs. Medicare Advantage: Key Differences

| Feature | Medigap (Supplement) | Medicare Advantage (Part C) |

|---|---|---|

| Works with | Original Medicare | Replaces Original Medicare |

| Provider network | Any doctor accepting Medicare | Usually limited network |

| Monthly premiums | Higher | Often $0 (but cost-sharing applies) |

| Out-of-pocket costs | Low and predictable | Varies; can be high for major events |

| Drug coverage included | No (need separate Part D) | Usually included |

| Extra benefits (dental, vision) | No | Often included |

| Works anywhere in the U.S. | Yes | Usually limited by service area |

Compare Medicare Advantage vs. Original Medicare with Medigap →

Frequently Asked Questions About Medigap Plans in 2026

What is the most popular Medicare Supplement plan in 2026?

Plan G is the most popular Medigap plan, with approximately 39% of all Medigap enrollees. It offers the most comprehensive coverage available to people who became eligible for Medicare on or after January 1, 2020.

Can I buy a Medigap plan if I already have Medicare Advantage?

You can apply for a Medigap plan, but you’ll need to drop your Medicare Advantage plan first and return to Original Medicare. In most states, you may be subject to medical underwriting unless you qualify for guaranteed issue rights.

Do Medigap plans cover prescription drugs?

No. Medigap plans do not cover prescription drugs. You’ll need to enroll in a separate Medicare Part D prescription drug plan for drug coverage.

What is the Part B deductible for 2026?

The annual Medicare Part B deductible is $283 in 2026. This is the amount you pay out of pocket before your Medigap plan (other than Plan C or F) covers Part B costs. Plans C and F cover this deductible, but are only available to those eligible for Medicare before January 1, 2020.

Can I switch Medigap plans after my Open Enrollment Period?

You can apply to switch plans at any time, but in most states, the insurance company can use medical underwriting to decide whether to accept your application and what rate to charge. Some states offer additional protections, such as annual open enrollment windows or birthday rules.

Are Medigap premiums tax-deductible?

Medigap premiums may be tax-deductible as a medical expense if your total medical expenses exceed 7.5% of your adjusted gross income. Consult a tax professional for your specific situation.

What is the difference between Plan G and Plan N?

Plan G covers Part B excess charges and has no copays for office or ER visits. Plan N does not cover Part B excess charges and requires copays of up to $20 for some office visits and up to $50 for ER visits that don’t result in admission. Plan N typically has lower monthly premiums than Plan G.

How do I find Medigap plans available in my state?

You can compare Medigap plans available in your area through Medicare.gov’s plan finder, or work with an independent Medicare advisor who can compare rates across carriers for your location.

Next Steps: Getting Help With Your Medicare Supplement Decision

Choosing a Medicare Supplement plan is one of the most important healthcare decisions you’ll make. The right plan can protect you from thousands of dollars in unexpected medical costs while giving you the freedom to see any doctor who accepts Medicare, anywhere in the country.

At The Big 65, we help Medicare beneficiaries across 33 states compare plans and carriers to find coverage that fits their needs and budget. As an independent advisory service not tied to any single insurance company, our guidance is focused on what’s right for you.

Related resources to help with your decision:

- How Much Does Medicare Supplement Plan G Cost?

- Medigap Plan G vs. Plan N: Detailed Comparison

- Best Medigap Insurance Companies

- Medicare Advantage vs. Original Medicare

- 2026 Medicare Costs: Complete Breakdown

- Complete Medicare Supplement Guide

👉 Ready to compare Medicare Supplement plans? Contact The Big 65 for free, personalized guidance.