If you are trying to understand Medicare costs in 2026, the hardest part is that there is no single Medicare bill. Your real cost depends on which parts of Medicare you use, whether you add a Medicare Supplement or Medicare Advantage plan, your prescriptions, your income, and how often you need care. The good news is that once you separate the costs by category, the picture gets much clearer.

Confused by your Medicare options? The Big 65 can help you compare your choices at no cost to you.

This guide gives you a complete 2026 Medicare cost breakdown in plain English. Use it as a budget checklist before you enroll, review your current coverage, or help a parent compare options.

Quick Summary: What Medicare Costs in 2026

Here are the major 2026 Medicare costs most people need to know first.

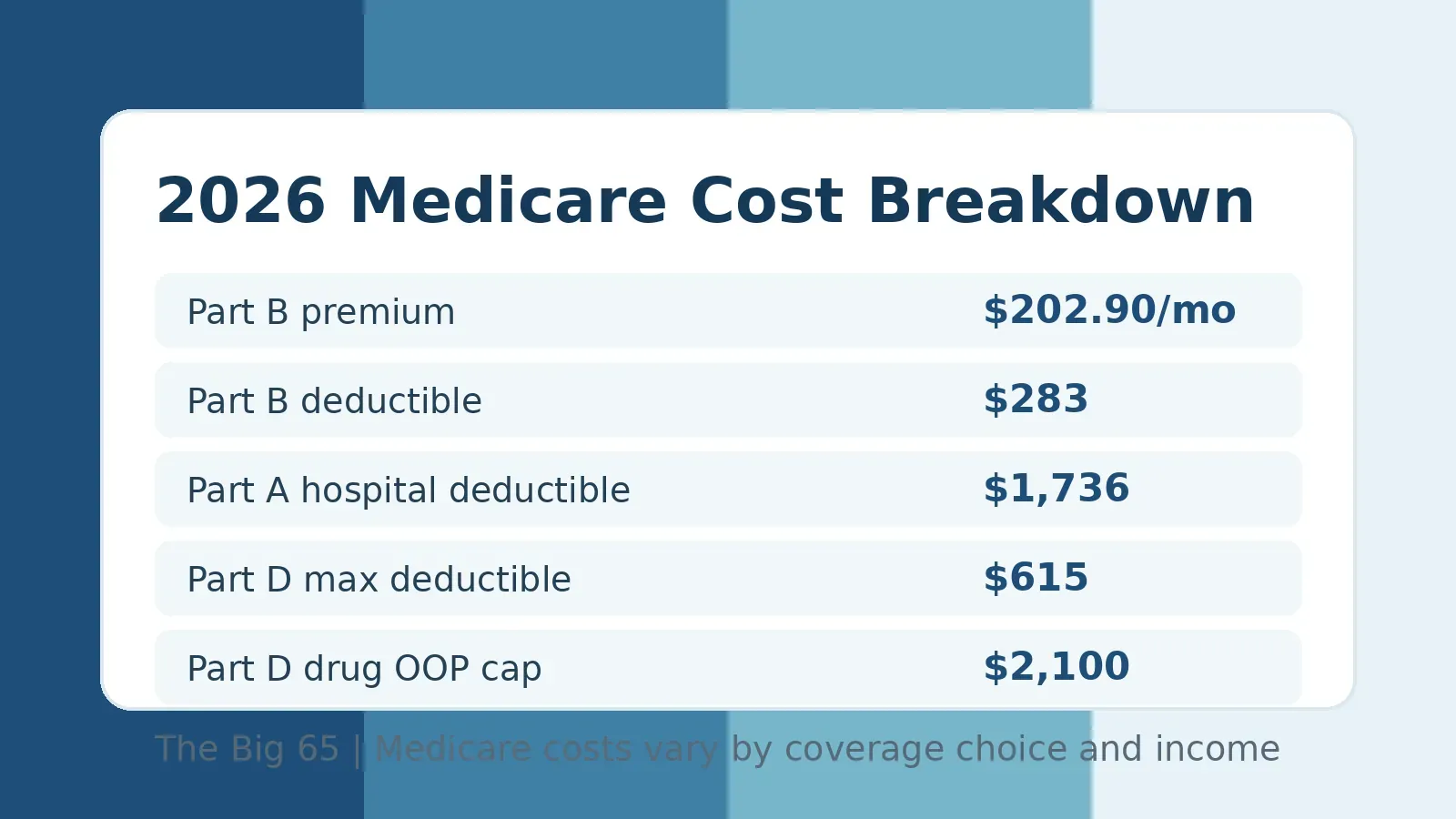

| Cost category | 2026 amount | What it means |

|---|---|---|

| Part B standard premium | $202.90 per month | The monthly premium most people pay for medical coverage |

| Part B deductible | $283 per year | What you pay before Part B generally begins paying its share |

| Part A inpatient hospital deductible | $1,736 per benefit period | Applies when you are admitted as an inpatient |

| Part D maximum deductible | $615 | No Medicare drug plan can have a deductible above this amount |

| Part D covered drug out-of-pocket threshold | $2,100 | After this, catastrophic coverage begins for covered Part D drugs |

These numbers are only the starting point. Your monthly budget can also include a Medicare Supplement premium, a Medicare Advantage premium, a Part D premium, dental or vision costs, copays, coinsurance, and costs for services Medicare does not cover.

What Costs Are Included in Medicare?

Medicare costs usually fall into seven buckets:

- Premiums: Monthly amounts you pay to keep coverage active.

- Deductibles: Amounts you pay before Medicare or your plan begins paying certain benefits.

- Copays: Fixed amounts for a service, visit, or prescription.

- Coinsurance: A percentage of the approved cost that you pay.

- Out-of-pocket maximums: Annual caps that apply to some plans, but not all parts of Medicare.

- Drug costs: Premiums, deductibles, and cost sharing for prescription medications.

- Non-covered services: Dental, vision, hearing, long-term care, and other services that may need separate planning.

The biggest mistake is comparing plans by premium alone. A low premium can still lead to higher total costs if your doctors are out of network, your prescriptions are expensive, or you need frequent care.

Medicare Part A Costs in 2026

Medicare Part A helps cover inpatient hospital care, skilled nursing facility care, hospice, and some home health care. Most people do not pay a Part A premium because they or a spouse worked long enough and paid Medicare taxes.

According to CMS, about 99% of Medicare beneficiaries do not pay a Part A premium. If you do not qualify for premium-free Part A, the 2026 monthly premium can be $311 or $565, depending on your work history.

| Part A cost | 2026 amount |

|---|---|

| Inpatient hospital deductible | $1,736 per benefit period |

| Hospital coinsurance, days 61 to 90 | $434 per day |

| Lifetime reserve days | $868 per day |

| Skilled nursing facility coinsurance, days 21 to 100 | $217 per day |

Part A costs can surprise people because the hospital deductible is per benefit period, not simply once per calendar year. If you want a deeper look at hospital-related costs, see The Big 65 guide to Medicare Part A hospital coverage and costs for 2026.

Medicare Part B Costs in 2026

Medicare Part B helps cover doctor visits, outpatient care, preventive services, durable medical equipment, and many medically necessary services outside the hospital.

For 2026, the standard Part B premium is $202.90 per month, and the annual Part B deductible is $283. After you meet the deductible, you typically pay 20% of the Medicare-approved amount for covered Part B services unless you have other coverage that helps pay that share.

Some people pay more for Part B because of IRMAA, which is an income-related monthly adjustment amount. Medicare generally looks at your tax return from two years prior to decide whether IRMAA applies. If your income has gone down because of retirement, marriage, divorce, loss of pension income, or another life-changing event, you may be able to ask Social Security to review the surcharge.

Original Medicare Has No Annual Out-of-Pocket Maximum

This is one of the most important cost details to understand. Original Medicare by itself does not have an annual out-of-pocket maximum for Part A and Part B services. That means your 20% Part B coinsurance can keep going if you have a year with major medical needs.

That is why many people add either a Medicare Supplement plan with Original Medicare or choose a Medicare Advantage plan. These two paths handle costs very differently.

Medicare Supplement Costs in 2026

Medicare Supplement insurance, also called Medigap, works with Original Medicare. You keep Original Medicare as your primary coverage and use the supplement to help pay some of the deductibles, coinsurance, and copays left behind.

The premium for a Medicare Supplement plan varies by state, age, ZIP code, tobacco status, household discounts, carrier, and plan letter. Plan G and Plan N are two of the most common choices for people new to Medicare.

- Plan G usually has a higher monthly premium than Plan N, but it covers more cost sharing after the Part B deductible.

- Plan N often has a lower premium, but you may have certain office visit and emergency room copays, and you may be responsible for Part B excess charges in states where they apply.

- Plan F is only available to people who were eligible for Medicare before January 1, 2020.

For a plan-by-plan comparison, review The Big 65 guide to Medicare Supplement Plan G vs Plan F vs Plan N. If you want to focus on one popular option, start with the Medicare Supplement Plan G guide.

Want help comparing Medigap premiums in your state? Ask The Big 65 for a no-cost Medicare review.

Medicare Advantage Costs in 2026

Medicare Advantage plans, also called Part C, are private Medicare plans that replace the way you receive Part A and Part B benefits. Many include Part D drug coverage. Some have low or even $0 premiums, but that does not mean the plan is free.

With Medicare Advantage, your costs usually come through copays, coinsurance, drug costs, and network rules. The plan must have an annual maximum out-of-pocket limit for covered Part A and Part B services. Once you hit that limit, the plan pays 100% of covered medical costs for the rest of the year. Prescription drugs have separate Part D rules.

When comparing Medicare Advantage costs, look at:

- The monthly plan premium

- Your primary care and specialist copays

- Hospital copays

- The annual medical out-of-pocket maximum

- Whether your doctors, hospitals, and pharmacies are in network

- How your prescriptions are covered

- Whether dental, vision, hearing, fitness, or transportation benefits are included

For more detail, read The Big 65 guide to Medicare Advantage costs in 2026 and the comparison of Medicare Advantage vs Medigap.

Medicare Part D Drug Costs in 2026

Medicare Part D helps pay for prescription drugs. You can get it through a stand-alone Part D plan with Original Medicare or through many Medicare Advantage plans that include drug coverage.

In 2026, no Medicare drug plan can have a deductible higher than $615. Some plans have a lower deductible or no deductible. After any deductible, many people pay copays or coinsurance based on the plan formulary and pharmacy network. Review our Part D prescription drug plan options if you want help comparing coverage choices.

For covered Part D drugs, Medicare.gov explains that the 2026 out-of-pocket threshold is $2,100. After your out-of-pocket spending on covered Part D drugs reaches that amount, catastrophic coverage begins. The Medicare Prescription Payment Plan may also let you spread your prescription drug costs across monthly payments instead of paying large amounts at the pharmacy counter all at once.

Drug costs are personal. A plan that is inexpensive for one person can be expensive for another if it does not cover the same medications well. Always compare plans using your exact prescriptions, dosages, and preferred pharmacies. The Big 65 has a separate guide to Medicare Part D prescription drug coverage in 2026.

Costs Medicare Usually Does Not Cover

Even a strong Medicare setup may leave gaps. Original Medicare generally does not cover most routine dental care, most routine vision care, hearing aids, long-term custodial care, cosmetic procedures, or care outside the United States except in limited situations.

Some Medicare Advantage plans include extra benefits for dental, vision, hearing, fitness, and other services. Some people keep Original Medicare and add separate dental, vision, or hearing coverage. The right path depends on your providers, health needs, budget, and comfort with networks.

How to Estimate Your Real Medicare Budget

To estimate what Medicare may cost you in 2026, do not stop at the government premiums. Build a full-year estimate with these steps:

- Start with Part B. Most people need to budget $202.90 per month for the 2026 standard Part B premium.

- Add Part A if needed. Most people pay $0, but not everyone qualifies for premium-free Part A.

- Choose your coverage path. Compare Original Medicare plus a Supplement and Part D against Medicare Advantage.

- Add plan premiums. Include Medigap, Part D, Medicare Advantage, dental, vision, and hearing premiums where applicable.

- Estimate routine care. Count expected doctor visits, specialist visits, therapy, lab work, imaging, and equipment.

- Run your prescription list. Check each drug against plan formularies and pharmacy pricing.

- Plan for a bad year. Compare what happens if you need a hospital stay, surgery, or expensive medication.

- Check income surcharges. If IRMAA applies, include the extra Part B and Part D amounts.

If you are turning 65, also read The Big 65 turning 65 Medicare enrollment guide so you do not miss key enrollment windows.

Which Medicare Cost Path Is Usually Best?

There is no universal winner. The best Medicare cost path depends on how you use care.

| If you value… | You may prefer… | Why |

|---|---|---|

| Predictable medical costs and broad provider access | Original Medicare plus a Medicare Supplement | You may pay a higher monthly premium, but fewer surprise medical bills |

| Lower monthly premiums and included extras | Medicare Advantage | You may accept networks and copays in exchange for a different cost structure |

| Specific doctor and hospital access | Depends on provider participation | Always verify your providers before choosing a plan |

| Expensive prescriptions | The plan that covers your drug list best | Drug formularies can change the total cost dramatically |

Because The Big 65 is an independent Medicare insurance brokerage, Karl Bruns-Kyler and the team can compare multiple Medicare products and explain tradeoffs without charging you a fee for the service. The premium is the same whether you use help or go directly to the insurance company.

Common Medicare Cost Questions for 2026

What is the standard Medicare Part B premium in 2026?

The standard Medicare Part B premium is $202.90 per month in 2026. Higher-income beneficiaries may pay more because of IRMAA.

What is the Medicare Part B deductible in 2026?

The Medicare Part B deductible is $283 in 2026. After the deductible, you typically pay 20% of the Medicare-approved amount for covered Part B services unless another plan helps pay that amount.

Does Medicare have a maximum out-of-pocket limit?

Original Medicare does not have an annual out-of-pocket maximum for Part A and Part B services. Medicare Advantage plans do have annual medical out-of-pocket limits for covered Part A and Part B services.

What is the maximum Part D deductible in 2026?

No Medicare Part D plan can have a deductible higher than $615 in 2026. Some plans have a lower deductible or no deductible.

Bottom Line on Medicare Costs in 2026

Medicare costs in 2026 include more than one premium or deductible. A realistic budget should include Part B, possible Part A costs, Medigap or Medicare Advantage costs, Part D drug costs, income-related surcharges, and services Medicare does not cover.

The best time to compare these costs is before you enroll or during an annual plan review. A plan that looked affordable at first glance may not be the best fit once you add prescriptions, providers, hospital risk, and annual out-of-pocket exposure.

Need help making sense of your 2026 Medicare costs? Contact The Big 65 for no-cost, one-on-one Medicare guidance.

Sources: 2026 Medicare Parts A and B premiums and deductibles from CMS; 2026 Part D deductible and out-of-pocket threshold information from Medicare.gov and CMS Part D guidance.

Not Sure Which Medicare Plan Is Right for You?

Medicare is complicated, but you do not have to figure it out alone. With over 20 years of experience, Karl Bruns-Kyler can help you compare plans, avoid costly mistakes, and find the coverage that fits your needs and budget.

Call (877) 850-0211

Or schedule a free consultation at a time that works for you.

There is never a charge for my services. Your premium is the same whether you work with me or go direct.

Disclaimer: We do not offer every plan available in your area. Currently, we represent 10 organizations that offer 50 products in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.